Lessons for Forest Investment from Debt Data

I was on a call the other day with one of our peers (he may be reading this now), and he asked whether I was concerned about the future of my business given the political and regulatory shift away from ESG and sustainability.

His concern is understandable. The evidence comes quickly to mind: the US formally exiting the IPCC and UNFCCC and several US states outlawing the consideration of ESG factors in investment decisions (S&P Global, 2025). In Europe, we’re watching the now infamous Omnibus debate unfold – where the EU after introducing complex sustainability regulations for business, is beginning to scale them back.

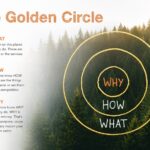

I’m not concerned about the sustainability umbrella remaining relevant in forest investment. All you need to do is look at the picture above.

For clarity, when I refer to this “umbrella,” I mean three closely related concepts:

- Sustainability – ensuring that economic, environmental and social value is maintained, now and into the future,

- ESG – material risk arising from environmental, social and governance factors,

- Impact – intentionally generating positive environmental and social outcomes alongside financial returns.

But in case you wanted evidence contrasting political signals – this study, titled Physical climate risk and the pricing of bank loans provides a counter argument. The study examines how physical climate risk affects the pricing of loans and finds a clear pattern: higher climate vulnerability – whether in a firm’s host country or where it operates subsidiaries – leads to higher borrowing costs. Loan pricing increases, loan sizes are adjusted, and additional collateral requirements and upfront fees are imposed to mitigate risk.

So what are the lessons for forest investment and sustainability?

To name just a few: this is a clear ESG risk for forest investment when we consider climate change and the exposure of forest assets to fire, drought, storms, and longer-term site–species mismatch. From a sustainability perspective, physical climate risk threatens predictable wood supply, forest health, and creates disproportionate negative consequences for Indigenous and forest-dependent communities.

Impact, however, represents the opportunity. It’s the chance to improve how forests are managed, protected, and restored in regions with high climate vulnerability—where those improvements can be linked to new markets, stronger returns, and access to investors seeking climate mitigation and adaptation strategies.

But here’s the key point: to leverage the impact opportunity—and to sustain the forest values that matter to us—we must manage ESG risk first. Without that, investors may simply discount forest opportunities in the same way debt investors are already doing – or worse, not invest at all.

Isn’t that something worth paying attention to?

Do you think ESG is dead in forest investment? Let me know your thoughts and what you’re seeing in your neck of the woods. And if you need support building or revising your sustainability strategy, please reach out.

Did you like this article? Sign up now for the ForestLink’s newsletter, where you’ll receive technical advice, reflections, and best-practice guidance to support you with your forest-linked investment strategy or business straight to your inbox.